Posts in category 'Real Estate News'

RSS Feed

RSS Feed

-

2026 | 2 Posts

- January | 2 Posts

- 2025 | 19 Posts

- 2024 | 29 Posts

- 2023 | 41 Posts

- 2022 | 36 Posts

- 2021 | 24 Posts

24

First-Time Home Buyer Share Falls to Historic Low of 21%, Median Age Rises to 40

Approximately nine in 10 buyers and sellers worked with a real estate agent, with seller representation reaching record highs.

17

Why More Homeowners Are Giving Up Their Low Mortgage Rate

If you're like a lot of homeowners, you've probably thought: "I'd like to move… but I don't want to give up my 3% rate." That's fair. That rate has been one of your best financial wins – and it can be hard to let go. But here's what you need to remember...

A great rate won't make up for a home that no longer works for you. Life changes, and sometimes, your home needs to change with it. And you're not the only one making that choice.

The Lock-In Effect Is Starting To Ease

Many homeowners have been frozen in place by something the experts call the lock-in effect. That's when you won't move because you don't want to take on a higher rate on your next home loan. But

19

Why You Don't Need To Be Afraid of Today's Mortgage Rates

Mortgage rates have been the monster under the bed for a while. Every time they tick up, people flinch and say, "Maybe I'll wait." But here's the twist. Waiting for that perfect 5-point-something rate could end up haunting your wallet later.

The Magic Number

According to the National Association of Realtors (NAR):

". . . a 30-year fixed rate mortgage of 6% would make the median-priced home affordable for about 5.5 million more households—including 1.6 million renters. If rates were to hit that magic number, it's likely that about 10%—or 550,000—of those additional households would buy a home over the next 12 or 18 months.

12

Why Experts Say Mortgage Rates Should Ease Over the Next Year

You want mortgage rates to fall – and they've started to. But is it going to last? And how low will they go?

Experts say there's room for rates to come down even more over the next year. And one of the leading indicators to watch is the 10-year treasury yield. Here's why.

The Link Between Mortgage Rates and the 10-Year Treasury Yield

For over 50 years, the 30-year fixed mortgage rate has closely followed the movement of the 10-year treasury yield, which is a widely watched benchmark for long-term interest rates (see graph below):

5

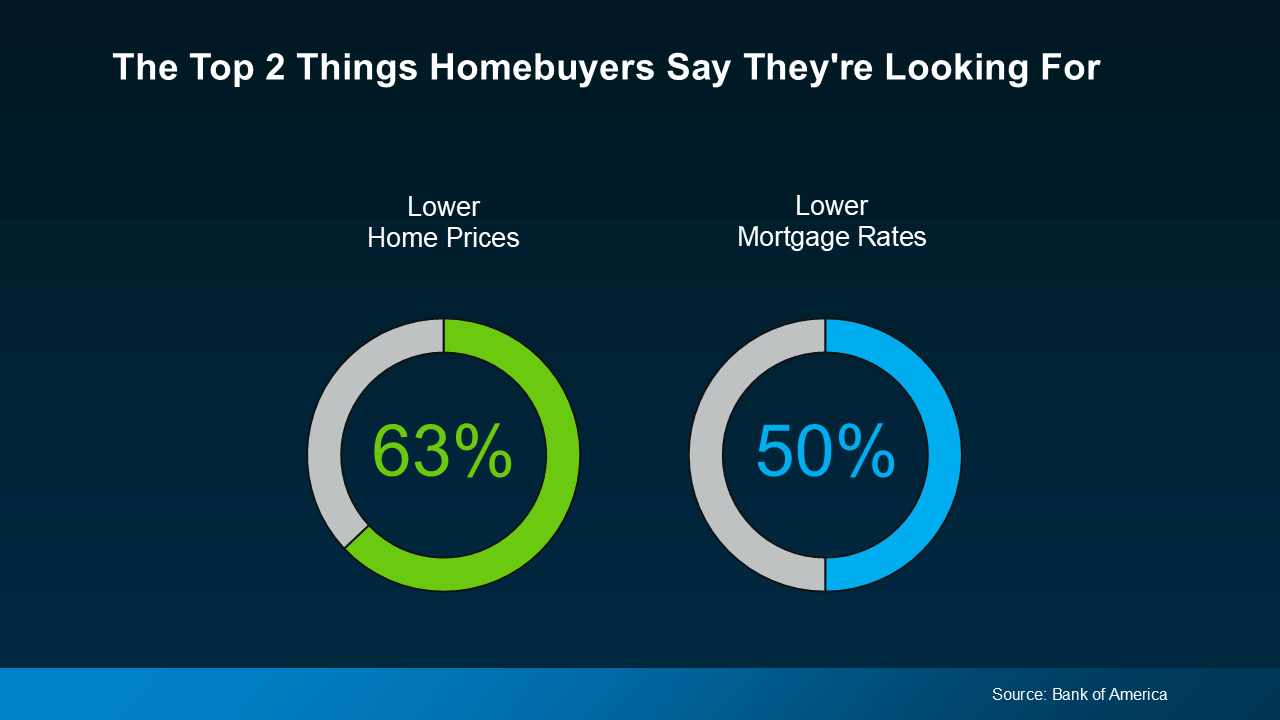

What Buyers Say They Need Most (And How the Market's Responding)

A recent survey from Bank of America asked would-be homebuyers what would help them feel better about making a move, and it's no surprise the answers have a clear theme. They want affordability to improve, specifically prices and rates (see below):

Here's the good news. While the broader economy may still fee...