Be In The Know

RSS Feed

RSS Feed

-

2026 | 2 Posts

- January | 2 Posts

- 2025 | 19 Posts

- 2024 | 29 Posts

- 2023 | 41 Posts

- 2022 | 36 Posts

- 2021 | 24 Posts

1

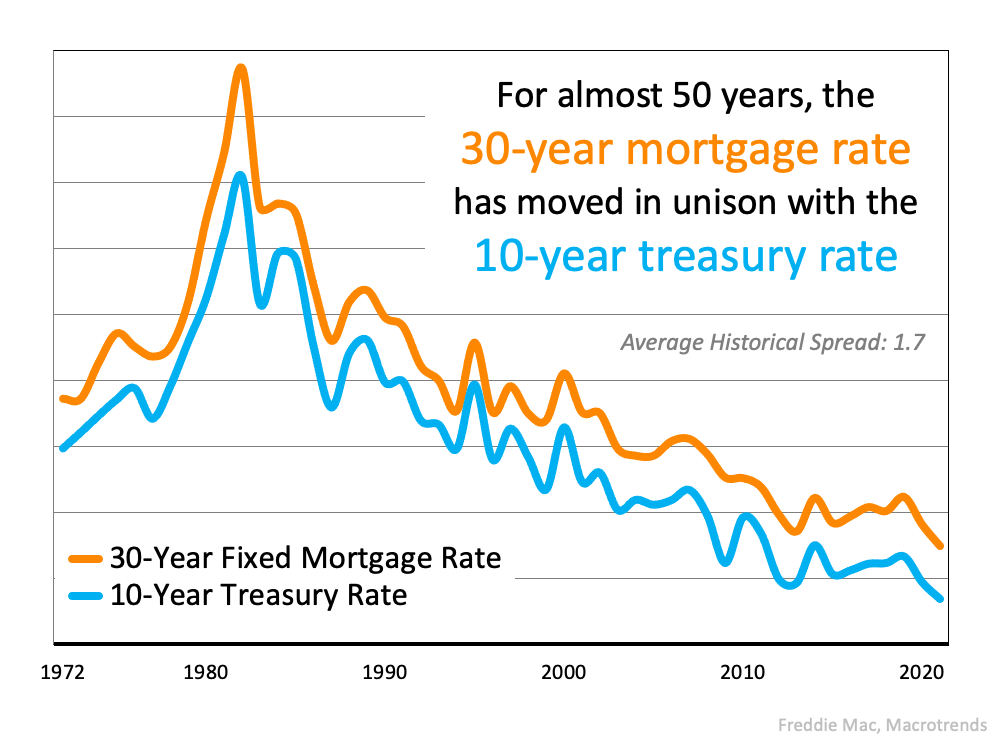

The Main Key to Understanding the Rise in Mortgage Rates

Every Thursday, Freddie Mac releases the results of their Primary Mortgage Market Survey which reveals the most recent movement in the 30-year fixed mortgage rate. Recently, it was the first time in three months that the mortgage rate surpassed 3%. In a press release accompanying the survey, Sam Khater, Chief Economist at Freddie Mac, explains:

"Mortgage rates rose across all loan types this week as the 10-year U.S. Treasury yield reached its highest point since June."

The reason Khater mentions the 10-year U.S. Treasury yield is because there has been a very strong relationship between the yield and the 30-year mortgage rate over the last five decades. Here's a graph showing that relationship:

The relationship has also been consistent throughout...

4

What Buyers and Sellers Need to Know About the Appraisal Gap

It's Economy 101 – when supply is low and demand is high, prices naturally rise. That's what's happening in today's housing market. Home prices are appreciating at near-historic rates, and that's creating some challenges when it comes to home appraisals.

In recent months, it's become increasingly common for an appraisal to come in below the contract price on the house. Shawn Telford, Chief Appraiser for CoreLogic, explains it like this:

"Recently, we observed buyers paying prices above listing price and higher than the market data available to appraisers can support. This difference is known as 'the appraisal gap . . . .'"

Why does an appraisal gap happen?

Basically, with the heightened buyer demand, purchasers...

27

The Best Use of Time and Money When it Comes to Renovations

In the current sellers' market, many homeowners wonder what, if anything, needs to be remodeled before they list their house. That's where a trusted real estate professional comes in. They can help you think through today's market conditions and how they impact what you should – and shouldn't – renovate before selling.

Here are some considerations a professional will guide you through:

1. With current supply challenges, buyers may be willing to take on projects of their own.

A more balanced market typically sees a 6-month supply of homes for sale. Above that, and we're in a buyers' market. Below that, and we're in a sellers' market. According to a recent report by the National Association of Realtors (NAR), our current supply of homes for sale, while rising, still...

20

More Young People are Buying Homes

There's a common misconception that younger generations aren't interested in homeownership. Many people point to the fact that millennials put off purchasing their first home as a reason for this belief.

Odeta Kushi, Deputy Chief Economist for First American, explains why millennials have put off certain milestones linked to homeownership.

Those delays led to their homeownership rates trailing slightly behind older generations:

"Historically, millennials have delayed the critical lifestyle choices often linked to buying a first home, including getting married and having children, in order to further their education. This is clear in cross-generational comparisons of homeownership rates which show millennials lagging their generational predecessors."

So, it's partially true...

13

A Look at Housing Supply and What it Means for Sellers

One of the hottest topics of conversation in today's real estate market is the shortage of available homes. Simply put, there are many more potential buyers than there are homes for sale. As a seller, you've likely heard that low supply is good news for you. It means your house will get more attention, and likely, more offers. But as life begins to return to normal, you may be wondering if that's something that will change.

While it may be tempting to blame the pandemic for the current inventory shortage, the pandemic can't take all the credit. While it did make some sellers hold off on listing their houses over the past year, the truth is the low supply of homes was years in the making. Let's look at the root cause and what the future holds to uncover why now is still a great time to sell.